Katherine Magee, J.P. Morgan Asset Management, Beta Investment Specialist.

Index-tracking strategies provide exchange-traded fund (ETF) investors with quick, scalable and cost-effective access to a broad range of global markets and asset classes. However, not all index funds are created equal, warns Katie Magee of J.P. Morgan Asset Management ETFs. Investors therefore need to fully understand the risks and opportunities provided by different types of index funds before they decide on the best approach for their portfolios.

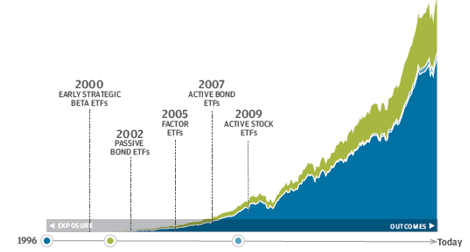

Index-tracking strategies are the bedrock of ETF investing, accounting for some $4.5 trillion of the $4.7 trillion global ETF industry (Morningstar data as of 24 March 2019).

Most of these assets (around $3.4 trillion) are in pure passive strategies that track traditional market capitalisation weighted indices.

Market cap weighting is simply the process of building an index based on the size of its constituents. In an equity index, bigger companies make up more of the index, while smaller companies make up less. In bond indices, the biggest debt issuers (in other words the biggest borrowers) make up most of the index.

By tracking market cap weighted indices, passive ETFs can offer efficient, low-cost, transparent and scalable exposure to global equity and bond markets—attributes that help explain the explosive growth in assets that these funds have experienced over the last 10 years.

Source: Morningstar. Data from 31 December 1996 to 24 March 2019.

As can be seen from the previous graph, index funds dominate ETF assets—and for a good reason. They provide cheap, efficient and scalable exposure to global markets.

However, while market cap weighted indices play a crucial role in many diversified portfolios, they do suffer from some well publicised limitations.

Equity indices are proportionally more concentrated in the stocks, sectors and regions that have performed well in the past, not necessarily those that will perform well in the future, while bond indices are biased towards the most indebted issuers, not necessarily the most solvent.

These inherent biases constitute unrewarded risks that investors may want to control their exposure to, or even eliminate entirely when investing in less liquid or less efficient markets.

An alternative, risk-aware approach to passive investing is provided by smart (or strategic) beta ETFs. These funds track indices that use criteria other than the company or issuer size to determine portfolio holdings.

Some indices weigh constituents or issuers equally, while some screen for securities with specific characteristics—such as low valuations, strong earnings or price momentum, or credit quality. And some do both.

The aim is to provide investors with cost-effective, passive exposure to specific markets and asset classes while addressing the objectives of the end investor and reducing the risks inherent in market cap weighted indices.

A good example of the advantages of a more risk-aware approach to indexation is provided by emerging market debt—an asset class that has seen large inflows as investors hunt for higher yields in the current low interest rate environment, attracted by the rising credit quality of emerging market issuers.

Several ETF providers offer exposure to emerging market debt through debt-weighted indices. However, there are some important reasons why, in the case of emerging market debt, using a traditional index may not be the best way to gain exposure to the asset class:

• First, debt-weighted indices are agnostic to the dangers posed by individual issuing nations, potentially exposing investors to significant country-specific risk; • Second, the characteristics of debt-weighted indices are driven entirely by debt issuance, meaning that credit ratings or duration exposures can change dramatically over time, regardless of the investor’s objectives; • Third, market cap weighted indices contain many smaller, less liquid bonds that do not necessarily impact returns but can significantly impact transaction costs.

Some ETF providers have attempted to address the challenges inherent in traditional emerging market debt indices by applying liquidity filters to exclude bonds with a short time to maturity or those with a relatively low face value.

Others have tilted the portfolio towards higher quality issuers, reducing country-specific credit risk but also reducing the portfolio’s yield.

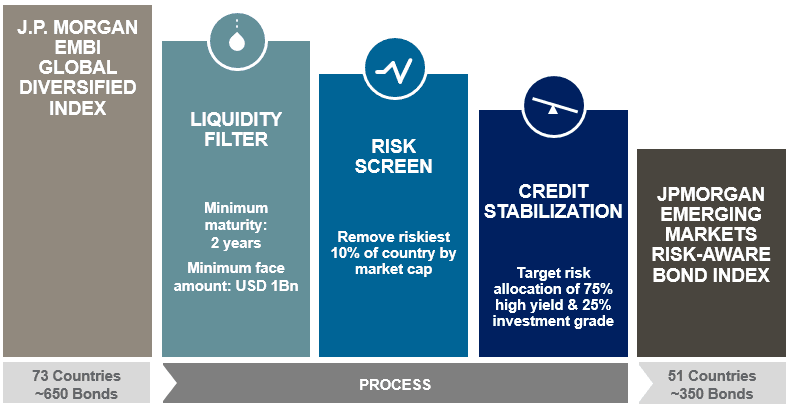

However, a liquidity screen only deals with one of the weaknesses of market cap weighted emerging market debt indices. That’s why we’ve designed our JPM USD Emerging Markets Sovereign Bond UCITS ETF (JPMB) to track the JPM Emerging Market Risk Aware Bond Index—an innovative benchmark that not only applies a liquidity screen, but also employs a risk screen to remove the 10% of the index by market cap that is at highest risk of default, and a credit stabilisation filter to ensure that 75% of the risk of the index is driven by high yield.

As can be seen in the graph to the right risk filters seek to reduce volatility, boost yield and avoid country specific risk compared to traditional indices.

These filters have helped the risk aware index to reduce sovereign default risk (Venezuela, for example, has been excluded since 2010), maintain high levels of liquidity and deliver a competitive yield compared to debt-weighted indices, and compared to other approaches that focus only on liquidity, or only on quality screening (which can lead to a lower yield).

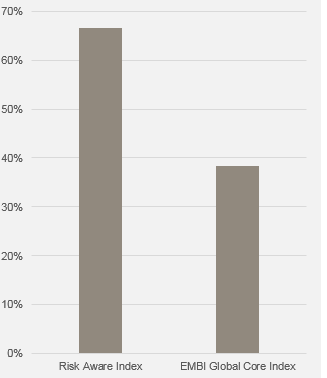

Since its inception on 31 December 2009, the risk-aware index has consistently outperformed the JPM EMBI Global Diversified Index (a commonly tracked debt-weighted benchmark) with lower volatility, providing investors with more consistency of performance.

The risk-aware index has also delivered a high rolling two-year batting average vs. the EMBI Diversified Index, outperforming the debt-weighted benchmark nearly 70% of the time.

The result is the opportunity to achieve lower volatility emerging market debt index exposure with more consistent returns.

Source: J.P. Morgan Asset Management. Target risk and return figures are the investment manager’s internal guidelines only. There is no guarantee that these objectives will be met.

Index funds provide quick, scalable and cheap market exposure to a wide range of markets and asset classes, many of which can otherwise be less easy to access. These attributes are the key to their huge popularity with investors over the last decade.

However, particularly in less liquid and less efficient markets, it’s important to choose the most appropriate index approach. Otherwise, investors can potentially be exposed to significant unintended portfolio biases and greater unrewarded risk concentrations than they perhaps bargained for.

As the example of JPMB shows, there are now many innovative ways to access markets using a strategic beta approach. When it comes to ETFs, passive should no longer automatically mean market cap weighted.

Bryon Lake, Managing Director, Head of International ETFs on improving in the ETFs industry.

This is a marketing communication and as such the views contained herein do not form part of an offer, nor are they to be taken as advice or a recommendation, to buy or sell any investment or interest thereto. Reliance upon information in this material is at the sole discretion of the reader. Any research in this document has been obtained and may have been acted upon by J.P. Morgan Asset Management for its own purpose. The results of such research are being made available as additional information and do not necessarily reflect the views of J.P. Morgan Asset Management. Any forecasts, figures, opinions, statements of financial market trends or investment techniques and strategies expressed are, unless otherwise stated, J.P. Morgan Asset Management’s own at the date of this document. They are considered to be reliable at the time of writing, may not necessarily be all-inclusive and are not guaranteed as to accuracy. They may be subject to change without reference or notification to you. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested. Changes in exchange rates may have an adverse effect on the value, price or income of the products or underlying overseas investments. Past performance and yield are not a reliable indicator of current and future results. There is no guarantee that any forecast made will come to pass. Furthermore, whilst it is the intention to achieve the investment objective of the investment products, there can be no assurance that those objectives will be met. J.P. Morgan Asset Management is the brand name for the asset management business of JPMorgan Chase & Co. and its affiliates worldwide. To the extent permitted by applicable law, we may record telephone calls and monitor electronic communications to comply with our legal and regulatory obligations and internal policies. Personal data will be collected, stored and processed by J.P. Morgan Asset Management in accordance with our EMEA Privacy Policy www.jpmorgan.com/emea-privacy-policy.

As the product may not be authorised or its offering may be restricted in your jurisdiction, it is the responsibility of every reader to satisfy himself as to the full observance of the laws and regulations of the relevant jurisdiction. Prior to any application investors are advised to take all necessary legal, regulatory and tax advice on the consequences of an investment in the products. Shares or other interests may not be offered to or purchased directly or indirectly by US persons. All transactions should be based on the latest available Prospectus, the Key Investor Information Document (KIID) and any applicable local offering document. These documents together with the annual report, semi-annual report and instrument of incorporation, are available free of charge from JPMorgan Asset Management (Europe) S.à r.l., 6 route de Trèves, L-2633 Senningerberg, Grand Duchy of Luxembourg, your financial adviser or your J.P. Morgan Asset Management regional contact or at www.jpmorganassetmanagement.ie. Units in Undertakings for Collective Investment in Transferable Securities (“UCITS”) Exchange Traded Funds (“ETF”) purchased on the secondary market cannot usually be sold directly back to UCITS ETF. Investors must buy and sell units on a secondary market with the assistance of an intermediary (e.g. a stockbroker) and may incur fees for doing so. In addition, investors may pay more than the current net asset value when buying units and may receive less than the current net asset value when selling them. In Switzerland, JPMorgan Asset Management (Switzerland) LLC, Dreikönigstrasse 37, 8002 Zurich, acts as Swiss representative of the funds and J.P. Morgan (Suisse) SA, 8 Rue de la Confédération, 1204 Geneva, as paying agent of the funds. JPMorgan Asset Management (Switzerland) LLC herewith informs investors that with respect to its distribution activities in and from Switzerland it receives commissions pursuant to Art. 34 para. 2bis of the Swiss Collective Investment Schemes Ordinance dated 22 November 2006. These commissions are paid out of the management fee as defined in the fund documentation. Further information regarding these commissions, including their calculation method, may be obtained upon written request from JPMorgan Asset Management (Switzerland) LLC. This communication is issued in Europe (excluding UK) by JPMorgan Asset Management (Europe) S.à r.l., 6 route de Trèves, L-2633 Senningerberg, Grand Duchy of Luxembourg, R.C.S. Luxembourg B27900, corporate capital EUR 10.000.000. This communication is issued in the UK by JPMorgan Asset Management (UK) Limited, which is authorised and regulated by the Financial Conduct Authority. Registered in England No. 01161446. Registered address: 25 Bank Street, Canary Wharf, London E14 5JP.

Source: J.P. Morgan Asset Management, Bloomberg. As at 30 April 2019. Index inception date: 31 December 2009. Indices do not include fees or operating expenses. Past performance is not a reliable indicator of current and future results.