David Zahn, CFA, FRM, Head of European Fixed Income, Franklin Templeton Fixed Income Group.

In this article David Zahn, Head of European Fixed Income, discuss the main aspects of the green bond sector.

Several initiatives have been launched to assist issuers, investors, banks and regulators in characterising green bonds. The International Capital Market Association (ICMA) has laid out a set of voluntary Green Bond Principles (GBPs). These were designed to improve transparency and set standards for disclosure in the green bond market. The Climate Bond Initiative (CBI) was set up to develop a taxonomy and a standard set of principles, along with a third-party certification scheme. Bond rating agencies have also launched products providing analysis of the green credentials of specific issues. These initiatives are voluntary and not legally binding.

Investors can use green and climate-aligned bonds to marry an investment outcome with sustainability goals. The issuer needs to balance the upfront costs of structuring a bond as green and the ongoing cost of compliance against the benefits of gaining access to investors interested in green bonds.

The definition of what qualifies as a green bond is not straightforward. The GBPs are voluntary, but in order to begin to understand what constitutes green financing and the process for whether an instrument complies with the GBPs, it is worth looking at the four components of the Principals:

1. Use of Proceeds (UOP). This needs to be adequately defined in the bond prospectus. In standard bonds, the UOP is often just stated as “General Corporate Purposes.” To be considered as green, at a minimum the UOP should clearly indicate the projects financed or refinanced by the proceeds and why these projects are environmentally beneficial. 2. Process for Project Evaluation. This includes a description of the issuer's sustainability objectives, its process for determining the eligibility of a project as green, and the process for managing environmental and social risks. 3. Management of Proceeds. Proceeds from green issuance need to be virtually segregated and linked to the green projects in a credible way. 4. Reporting. The issuer should regularly provide up-to-date information on the progress of the projects detailed in the UOP.

The GBPs recommend external reviews, and this has certainly emerged as best practice in the industry. External certification is meant to support transparency pre-issue and in ongoing reporting. There are several types of external reviews, including:

• 'Second-party opinion' from an organisation that is an expert in environmental sustainability and is sufficiently independent of the issuer to be credible. • 'Verification' from an independent operator should be measured against a designated set of criteria, usually focused on the environment and sustainability. • 'Certification' from accredited third parties confirms alignment with a stated green bond standard. It does not make a judgement on the “greenness” of the bond. • 'Rating' from specialised research providers or agencies that typically judges the 'greenness' of the bond.

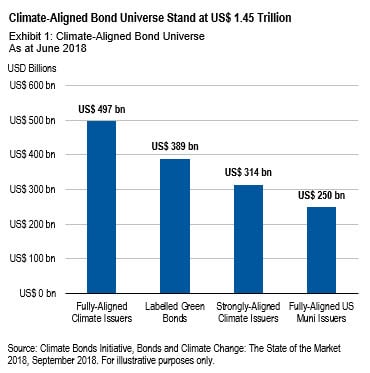

Pure-play issuers are companies that earn all or most of their revenues from green activities. The CBI defines a company deriving 75%–95% of revenues from green business lines as “strongly climate-aligned,” but to be “fully climate-aligned” a company needs to derive 95% or more of its revenues from green business lines. Qualifying business lines are those that are designed to help deliver a low-carbon and climate-resilient economy.1

Repayment of most green bonds comes not from one successful project, but from the cash flows generated by the issuer. Satisfaction with the issuer’s ability to repay is the first fence any investment must hurdle.

In the event of a financial restructuring, there is no automatic additional claim on the assets of the company simply as a result of a green label.

Fundamental analysis can then be allied to a top-down review of a company’s carbon neutralisation plans and its general climate engagement strategy, which in turn gives insight into the environmental sustainability of that company’s business model.

Taken together, these analyses form a rounded view as to the suitability of an individual bond for inclusion in a diversified credit portfolio.

The European Commission has proposed €45 billion a year be dedicated to climate projects in the next budget (2021–2027), representing around 25% of the total.

There are two further pieces of legislation due to be presented in the near term: - Investor duties and disclosures—asset managers and institutional investors need clarity on what duties they have for taking sustainability into account in both their investment process and disclosure requirements. - The creation of two new categories of benchmark to improve transparency and to avoid suspicions of “green-washing”: 1. low-carbon or decarbonised version of standard indices. 2. positive-carbon impact benchmark that will allow portfolios to be better aligned with the Paris Agreement objective of limiting global warming to below 2° Celsius.

A mixture of corporate, sovereign and EU-backed bonds may be needed to bridge the gap between the investment backed by the EU budget and the required total. Policymakers are also keen to persuade investors to support much longer-term issuance to better match asset lives, and this may require incentivisation.

In terms of demand, green issuances are oversubscribed. We believe this suggests that the size of the investor base interested in supporting the transition to a lower-carbon economy is significant. Data from the CBI for the first half of 2018 showed 72% of green bonds had tighter spreads than ordinary bonds after seven days, and 62% were tighter after 28 days.

In our opinion, this implies that there is very strong demand for these bonds in the secondary market. In periods of risk aversion, anecdotal evidence has suggested green bonds may exhibit lower volatility as investors tend to hold on to these bonds.

Lower volatility could also create opportunities for active managers to switch into bonds at longer maturities, with consequently higher spreads, without having an unacceptable impact on potential short-term volatility.

Watch David speak live from FundForum International 2019 here.

Green bonds are already a key tool in the attempt to decarbonise the global economy and are set to see continued rapid growth.

The climate ambitions of the EU alone will require investment of €180 billion annually over the next decade, but only a portion of these bonds will be eligible for inclusion in indices.

We believe a well-balanced green bond portfolio should have a wider remit, otherwise the debt of companies that are crucial to the growth of the low-carbon economy will be excluded. Hence, an active approach to investing in green bonds allows a portfolio manager to apply discretion while still investing in bonds that provide environmental benefits.

We believe this approach can also deliver compelling risk-adjusted return for clients.

Learn more about Franklin Liberty's Euro Green Bond UCITS ETF here.

1. Source: C2ES Centre for Climate and Energy Solutions.